Morningstar’s ‘Bucket Portfolio’ is typical of so-called Lazy Portfolios — static investing strategies that never change the percentages allocated to a set of index funds. Fortunately, with one easy fix, we can add an amazing 3½ percentage points to the annualized return of Morningstar’s portfolio. The answer demonstrates a basic use of the ‘momentum factor’ — a rule that economists have proven in hundreds of peer-reviewed studies.

This column is Part 2. Part 1 appeared on Nov. 6, 2018.

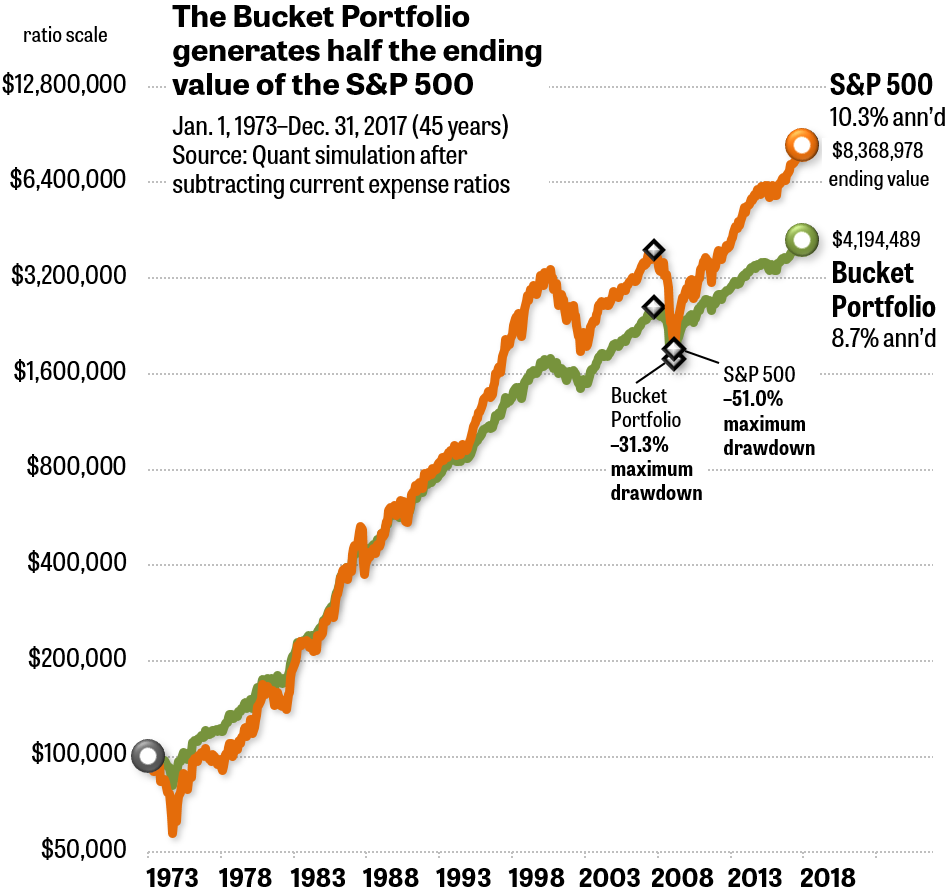

The graph above shows a 45-year simulation of the performance of Morningstar’s “Aggressive Bucket Retirement Portfolio.” As explained in my previous column, this investing strategy for 401(k) plans, IRAs, and brokerage accounts holds nine mutual funds in specific percentages at all times.

Because of the static allocations to each of the index funds, the Bucket Portfolio cannot adapt to market conditions. There is no formula to tilt the portfolio toward those assets that are in uptrends and out of assets that are in downtrends.

As a result, over the past 45 years, the Bucket Portfolio would have produced an ending value about half as much as a buy-and-hold of the S&P 500. (Both strategies include dividends.) Someone starting with $100,000 as a young person would end up with $4.19 million in the Bucket Portfolio but twice as much — $8.37 million — in the S&P 500. Naturally, someone in retirement could withdraw a lot more to live on from the index, which had an annualized rate of return of 10.3%, than the Bucket Portfolio with its return of only 8.7%.

Ending up with half the wealth at the end of a lifetime of investing might be justified if the Bucket Portfolio kept bear-market losses to a bare minimum. However, the Bucket’s worst loss, more than –31%, is beyond what many or most individual investors would tolerate. Yes, it’s better than the S&P 500’s –51% maximum drawdown. But losing more than 30% of your life savings still would compel a lot of people to liquidate their holdings to stop the emotional pain.

The graph above was generated by the Quant simulator. This program was developed by Mebane Faber, co-author of The Ivy Portfolio. I consider it a simulator rather than a backtester, because Quant contains no data on individual stocks. Instead, it’s one of the few tools that includes the actual performances of indexes such as developed-market stocks, REITs, commodities, bonds, etc. It also subtracts transaction costs and fees. The program can be requested from Faber as a free bonus upon a $399 subscription to his Idea Farm Newsletter.

Are the Quant simulations reliable? They’re a close approximation to what a strategy might do if markets continue to have rallies and crashes in the future, as they have for hundreds of years. Of course, four decades ago there were no index funds, and trading costs were not as low as they are today. But if we want to take advantage of modern index funds — and we definitely do — tools like Quant give us an objective way to compare strategies. All we can really say is that Strategy A might be better than Strategy B, which might be better than Strategy C, but that’s saying quite a lot. The returns of the future will never be exactly the same as in the past. Just consider Quant to be a comparative tool, not a crystal ball.

The construction of the Bucket Portfolio includes a weakness

One reason for the expected underperformance of the Bucket Portfolio is its large allocation of 8% to cash (such as a money-market fund). This stash of cash is intended to make individual investors “stay the course” during crashes rather than switching out of stocks during market panics. The idea is that a person or a couple who have two years’ worth of living expenses — safe in the bank — can ignore the plunges of 30% to 50% that the S&P 500 subjects investors to once every 10 years, on average.

In an interview, Morningstar director of personal finance Christine Benz explained that the 8% rule can be customized to fit different lifestyles. For example, a person who receives a large pension benefit in retirement might reduce the 8% cash cushion. Benz describes this kind of customization in an Aug. 8, 2016, article. (The Web page is behind Morningstar’s paywall, but many local libraries can give you free access.)

Does Benz know of any academic studies showing that holding 8% of one’s wealth in cash really prevents individuals from selling their stocks during a widespread panic? “No, I don’t,” she said. Her concept of three mental compartments — keeping 8% in cash, 35% in bond-like assets, and 57% in equity-like assets — is often said to originate from strategists such as Harold Evensky, as stated in a Sept. 19, 2016, Morningstar article.

Evensky, a financial adviser and co-author of The New Wealth Management, has his own ideas. In an interview with Robert Huebscher of Advisor Perspectives, Evensky said the three-bucket approach has some “really serious fatal flaws.” He pointed to the rebalancing requirements, transaction expenses, and tax drag as reasons the strategy is ineffective.

“It just does not seem practical or feasible, and no one has explained to me how it can be done,” Evensky said. He himself uses a simpler, two-bucket approach in his own practice.

Asked about Evensky’s critique, Benz replied: “He manages clients’ investments for them. My Bucket Portfolios are designed for individual investors to manage by themselves.”

The missing element in the Bucket Portfolio: momentum

Like all Lazy Portfolios, Morningstar’s Bucket Portfolio assumes that a specific allocation of assets should be held at all times. That subjects such portfolios to middling performance and, worse, deep crashes far beyond the 20% or 25% losses that many or most individuals can tolerate in their life savings. (For evidence, see my summary.)

For years, financial authorities thought mere diversification could provide superior returns as well as adequate protection against crashes. But in the early 1990s, researchers proved with academic rigor that assets with price gains in the past 3 to 12 months are statistically likely to rise for one more month.

This was called the “momentum factor” and became part of the well-known “four-factor model” documented by economists such as Eugene Fama, Kenneth French, and Mark Carhart. Recently, they’ve gone so far as to say, “All models that do not include a momentum factor fare poorly.” (Fama & French, 2014.) “This theory has been one of the most strongly tested in all of modern finance, with more than 300 academic and practical papers.” (Garff, 2014.)

What if you forget about the “three buckets” and add a momentum rule to Morningstar’s portfolio? At the beginning of each month, make sure you’re holding the three index funds (out of nine) that have the strongest momentum, based on their total return over the past 3, 6, and 12 months.

The result is amazingly robust. The momentum version of the Bucket Portfolio would have double the dollar gain of the Lazy Portfolio version within a matter of years. Over the entire 45-year period shown in the graph above, the momentum version would have an ending value more than four times that of the vanilla Bucket Portfolio, according to the Quant simulator. And your maximum drawdown during the 2007–2009 financial crisis would have been only –15%. That’s not even a bear market in your life savings!

In the next part of this column, we’ll see exactly how this simple step works to improve a portfolio and how we can best use it.

Parts 3 and 4 of this column appear on Nov. 13 and 15, 2018.

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com