Market Recap for Monday, October 1, 2018

The big news was the United States, Canada and Mexico agreeing to replace the North American Free Trade Agreement (NAFTA) and automobile manufacturers ($DJUSAU, +5.84%) were the clear winners. The group also benefited from a quick settlement between the SEC and Tesla's (TSLA, +17.35%) CEO Elon Musk for his infamous tweet regarding "funding secured" to take TSLA private. The SEC said Musk had no such funding in place and simply manipulated the price of TSLA's stock for which he, along with TSLA, each agreed to a $20 million fine. Musk was allowed to remain as CEO, but he was stripped of his Chairman role for at least three years. Many believe the penalties should have been much harsher, but with that cloud no longer hovering, TSLA regained all that it had lost on Friday (with respect to its stock price). Despite the new trade agreement, which still must be approved by all three countries, and the TSLA settlement, the DJUSAU remains in a downtrend and a significant underperformer in 2018:

Autos absolute and relative weakness is clearly depicted above. I wouldn't consider this group until we see the daily PPO move above its centerline. So long as it remains beneath it, bearish momentum is in play. The initial "knee-jerk" reaction to the new trade agreement was positive, but the DJUSAU must sustain yesterday's strength in order to right the ship. We could see further strength near-term, but the long-term looks weak to me.

Autos absolute and relative weakness is clearly depicted above. I wouldn't consider this group until we see the daily PPO move above its centerline. So long as it remains beneath it, bearish momentum is in play. The initial "knee-jerk" reaction to the new trade agreement was positive, but the DJUSAU must sustain yesterday's strength in order to right the ship. We could see further strength near-term, but the long-term looks weak to me.

General Electric (GE, +7.09%) had one of its best days over the past couple years as their CEO John Flannery was ousted after an uninspiring 1 year at the helm. GE stock lost half its market value during Flannery's tenure and the company remains in a technical tailspin despite the gain on Monday. The good news for new CEO Larry Culp is that it would be difficult for GE not to perform better than it did under Flannery's reign. Here's a long-term look at GE's performance:

Personally, it doesn't seem to me that one year is long enough to evaluate a CEO's performance. After all, GE acknowledged many problems when Flannery took over the helm. And many more problems surfaced in the year that he was CEO. But obviously GE shareholders grew impatient with the putrid absolute and relative performance of the company and the substantial cutting of its dividend. In that sense, Flannery suffered the fate of an NFL head coach that takes over an underachieving team and can't immediately turn the ship in his first year. The mess at GE took much longer than one year to create and I'd argue that Flannery probably should have been given more time to clean up the mess in order to properly assess his job performance. However, money talks and after a year in which shareholders lost half the value of their holdings, time wasn't on Flannery's side.

Personally, it doesn't seem to me that one year is long enough to evaluate a CEO's performance. After all, GE acknowledged many problems when Flannery took over the helm. And many more problems surfaced in the year that he was CEO. But obviously GE shareholders grew impatient with the putrid absolute and relative performance of the company and the substantial cutting of its dividend. In that sense, Flannery suffered the fate of an NFL head coach that takes over an underachieving team and can't immediately turn the ship in his first year. The mess at GE took much longer than one year to create and I'd argue that Flannery probably should have been given more time to clean up the mess in order to properly assess his job performance. However, money talks and after a year in which shareholders lost half the value of their holdings, time wasn't on Flannery's side.

While the overall Monday headlines dominated the action yesterday and the Dow Jones and S&P 500 ended with solid gains, strength wasn't as apparent as the headlines might suggest. The NASDAQ, higher by 60 points early in the trading day, finished with a small loss and small cap stocks (Russell 2000) were trounced, falling 23.58 points (-1.39%) to close at a six week low. Small caps have been shunned for several weeks now, even as the U.S. Dollar Index ($USD) has rebounded.

Pre-Market Action

Crude oil ($WTIC) is up fractionally to $75.40 per barrel after closing at a near 4 year high on Monday. Gold ($GOLD) is up 8 dollars this morning to once again hit the $1200 per ounce level. On a closing basis, GOLD has been trapped between $1180 and $1220 for several weeks and this morning's gains puts the yellow metal right back into the middle of this trading range.

Hong Kong's Hang Seng Index ($HSI) tumbled 662 points (-2.38%) overnight, although other Asian markets were able to close mostly higher. European markets are lower this morning, most likely in reaction to the selling in U.S. markets that took place in the second half of Monday's session.

Dow Jones futures are weak this morning, down 58 points with a half hour left to the opening bell.

Current Outlook

Crude oil ($WTIC, +2.80%) closed at $75.30 per barrel on Monday, its highest close since late 2014. The result was a surging energy group (XLE, +1.39%) that ended up leading the action on Monday. The good news is that the XLE tends to follow the $WTIC so the latter's breakout is likely to be followed by an XLE breakout as well:

Both crude and the XLE can be quite volatile, but both are clearly in an uptrend. The key for the XLE moving forward will be the ability for WTIC to remain above both its price and trendline support levels. They both intersect close to $64 per barrel. So long as that holds, the XLE should be considered as part of a diversified ETF portfolio. The XLE also will likely be a solid trading vehicle in the near-term given the WTIC breakout.

Both crude and the XLE can be quite volatile, but both are clearly in an uptrend. The key for the XLE moving forward will be the ability for WTIC to remain above both its price and trendline support levels. They both intersect close to $64 per barrel. So long as that holds, the XLE should be considered as part of a diversified ETF portfolio. The XLE also will likely be a solid trading vehicle in the near-term given the WTIC breakout.

Sector/Industry Watch

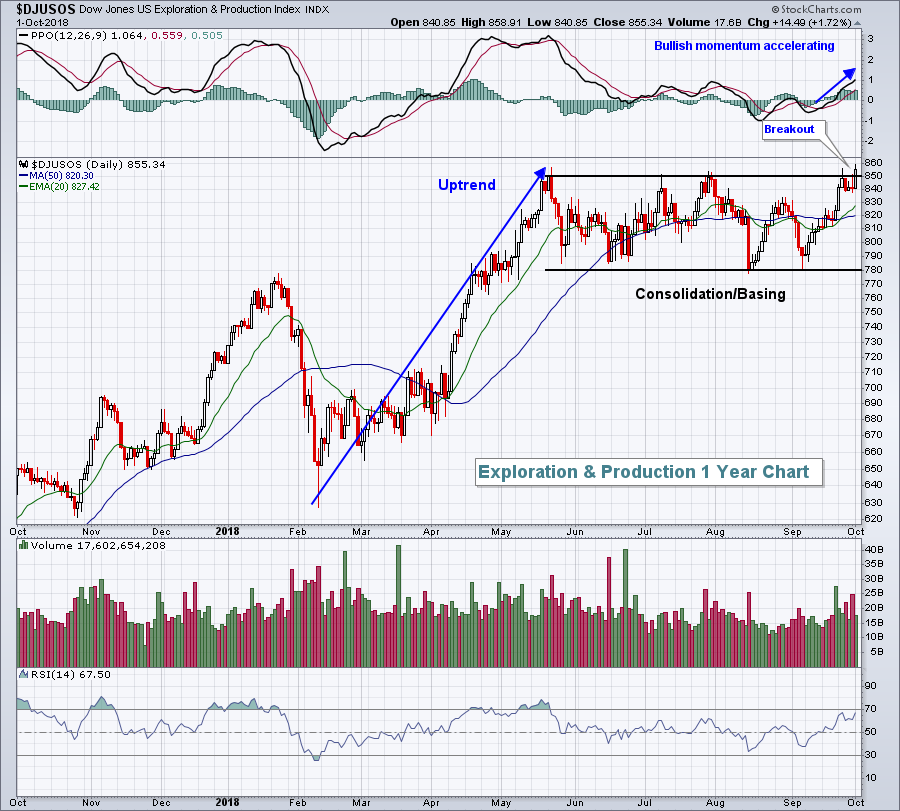

The Dow Jones U.S. Exploration & Production Index ($DJUSOS) has been the strongest industry within energy and the group made a significant breakout on Monday after basing for months:

There have been many disappointments technically in the energy space over the past few years, but the DJUSOS isn't one of them. The group consolidated beautifully off its most recent uptrend, then surged yesterday when crude oil broke out. This area remains solid for both short-term and intermediate-term trading.

There have been many disappointments technically in the energy space over the past few years, but the DJUSOS isn't one of them. The group consolidated beautifully off its most recent uptrend, then surged yesterday when crude oil broke out. This area remains solid for both short-term and intermediate-term trading.

Historical Tendencies

3M Co. (MMM) is threatening a breakout on its weekly chart as it heads into its most bullish seasonal period of the year:

A move above 220 would certainly begin to make a case for a bullish cup forming off a two year uptrend in which MMM nearly doubled its market cap. Seasonality only adds to the potential bullishness here as MMM has produced excellent results in October over the past two decades. In addition to averaging a 3.2% October gain over the past 20 years, MMM has risen 19 of the past 20 Novembers, producing an average November gain of 3.5%. That's an average two month gain (October/November) of 6.7%. Throw in MMM's annual dividend yield of 2.58% (.65% per quarter) and it represents a nice opportunity in a fairly stable stock. A Friday close beneath the rising 20 week EMA would be an indication to re-evaluate the trade.

A move above 220 would certainly begin to make a case for a bullish cup forming off a two year uptrend in which MMM nearly doubled its market cap. Seasonality only adds to the potential bullishness here as MMM has produced excellent results in October over the past two decades. In addition to averaging a 3.2% October gain over the past 20 years, MMM has risen 19 of the past 20 Novembers, producing an average November gain of 3.5%. That's an average two month gain (October/November) of 6.7%. Throw in MMM's annual dividend yield of 2.58% (.65% per quarter) and it represents a nice opportunity in a fairly stable stock. A Friday close beneath the rising 20 week EMA would be an indication to re-evaluate the trade.

Key Earnings Reports

(actual vs. estimate):

LW: .73 vs .68

PAYX: .65 (estimate - still awaiting results)

PEP: 1.59 vs 1.56

Key Economic Reports

None

Happy trading!

Tom