Market Recap for Tuesday, January 30, 2018

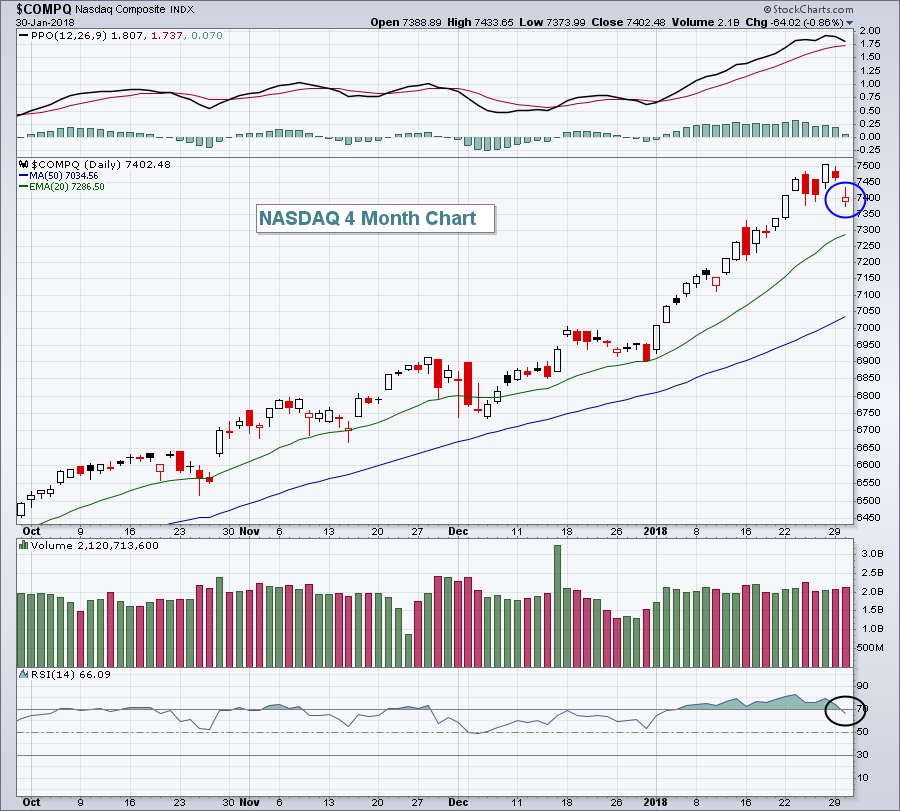

This day was a long time coming. The U.S. stock market's uninterrupted surge to record all-time highs day after day, week after week and month after month needed a break. It needed relief. Yesterday that relief was found....and it came in a hurry. We saw significant gaps lower on all of our major indices and we closed near the day's low on both the Dow Jones and S&P 500. Action on the NASDAQ was actually somewhat bullish as this tech-laden index finished with a slightly hollow candle, meaning that it closed above its open:

The move lower did break the strong January trendline higher, but we've yet to see even a 20 day EMA test since late-December. It's hard to think many bearish thoughts until we at least see a close beneath that key moving average. Note the black circle above that highlights the RSI falling beneath the overbought 70 level for the first time in 3 weeks. That blue circle, however, shows that buyers have not gone away. After early selling took the NASDAQ down more than 90 points, the bulls were able to cut into those losses in the afternoon session.

The move lower did break the strong January trendline higher, but we've yet to see even a 20 day EMA test since late-December. It's hard to think many bearish thoughts until we at least see a close beneath that key moving average. Note the black circle above that highlights the RSI falling beneath the overbought 70 level for the first time in 3 weeks. That blue circle, however, shows that buyers have not gone away. After early selling took the NASDAQ down more than 90 points, the bulls were able to cut into those losses in the afternoon session.

Healthcare stocks (XLV, -2.10%) were very weak after Amazon (AMZN), Berkshire Hathaway (BRK.A) and JPMorgan Chase (JPM) announced they were forming a new company - with no profit incentive - to explore better healthcare options for their employees. They are striving to improve employee satisfaction while lowering costs. That announcement spooked most drug distributors like Express Scripts (ESRX), managed care insurers like CIGNA (CI) and drug retailers like CVS Health Corp (CVS). The good news is that many of these healthcare companies finished well off their intraday lows as buyers found the gaps lower to be opportunites to buy rather than to sell.

All sectors, except utilities (XLU, +0.18%) finished lower on the day, but both consumer discretionary (XLY, -0.50%) and consumer staples (XLP, -0.67%) managed to avoid the heavier selling that other sectors experienced.

Pre-Market Action

Dow Jones futures (+217 with 45 minutes left to the open) are strong this morning, potentially eliminating a big chunk of Tuesday's losses at the opening bell.

The ADP Employment report came in much stronger than anticipated, aiding futures.

Boeing (BA) posted very strong quarterly results this morning before the bell, also aiding Dow Jones futures.

Current Outlook

Let's watch the Volatility Index ($VIX) - expected volatility - to see if it settles back down during rally attempts in equities. Bull markets thrive on low expected volatility. History tells me that the 16-17 level on the VIX is significant. The last two bear markets never saw a VIX reading below this level so the bears have two goals. First, they need to push the expected volatility level above this 16-17 range. Second, on any subsequent market rally, it must remain there. There must be a fear element for sellers to remain in charge. Bear markets don't start and can't survive in a low volatility environment. It's like waiting for snow in Key West, Florida. It ain't gonna happen.

As a reminder, here's a long-term look at how the VIX has performed just before and during the last two bear markets:

The red arrows above show that the VIX never moved below 16 during countertrend rallies on the S&P 500. In other words, fear remained elevated so a new bull market could never get started. The black circles show VIX readings well above 16-17 when the final market top occurred. Market tops do not historically occur when we have the kind of low VIX readings that we've experienced the past several years. Market tops don't just happen, they evolve over time. Also, a high VIX, by itself, does not mean bear market. Just as clouds in Key West don't mean snow. You still need cold temperatures. In the stock market, we need to see a rising VIX occur simultaneously with other bearish developments. One such development would be market rotation into defensive sectors. Check out the Sector/Industry Watch section below for an illustration.

The red arrows above show that the VIX never moved below 16 during countertrend rallies on the S&P 500. In other words, fear remained elevated so a new bull market could never get started. The black circles show VIX readings well above 16-17 when the final market top occurred. Market tops do not historically occur when we have the kind of low VIX readings that we've experienced the past several years. Market tops don't just happen, they evolve over time. Also, a high VIX, by itself, does not mean bear market. Just as clouds in Key West don't mean snow. You still need cold temperatures. In the stock market, we need to see a rising VIX occur simultaneously with other bearish developments. One such development would be market rotation into defensive sectors. Check out the Sector/Industry Watch section below for an illustration.

Sector/Industry Watch

The last time we saw the onset of a major market top in 2007, money rotated significantly towards defensive sectors as the S&P 500 attempted rallies to near the October 2007 high:

Those last attempts to continue the bull market failed miserably and a primary reason was that leadership during those failed rally attempts came from defensive groups. The blue directional lines to the right of the vertical line (at the time of the October 2007 top). Also note that the rally attempts all coincided with the VIX remaining at or above the 16-17 support area. These are just a couple of indications we need to follow as we decipher market action in the next several months/years.

Those last attempts to continue the bull market failed miserably and a primary reason was that leadership during those failed rally attempts came from defensive groups. The blue directional lines to the right of the vertical line (at the time of the October 2007 top). Also note that the rally attempts all coincided with the VIX remaining at or above the 16-17 support area. These are just a couple of indications we need to follow as we decipher market action in the next several months/years.

By the way, that final relative ratio at the bottom of my chart above is the XLY:XLP, my favorite ratio to assess the strength of any market rally. When the stock market is moving up, we want to see this ratio either move sideways or higher (preferred) so that we know traders are opting for the more aggressive discretionary side of consumer stocks. Note the exact opposite occurred in 2007 as traders braced for one of the worst bear markets in our history.

Historical Tendencies

The Russell 2000 historical performance is quite interesting when we consider how it performs during the calendar month. This stat is simply mind-boggling. Since 1987, here are the annualized returns for each of the calendar periods shown:

25th through 5th: +27.80%

6th through 24th: +0.38%

History tells us that the small caps are not worth the risk from the 6th calendar day of the month through the 24th. Your reward for holding small cap stocks for these 19 calendar days of each month for the past three decades? ZERO.

Key Earnings Reports

(actual vs. estimate):

ADP: .99 vs .89

ANTM: 1.29 vs 1.25

BA: 4.80 vs 2.91

CHKP: 1.58 vs 1.51

DHI: .77 vs .64

EPD: .37 vs .35

IR: 1.02 vs 1.02

JCI: .54 vs .51

LLY: 1.14 vs 1.08

SIRI: .05 vs .05

SPG: 3.12 vs 3.12

TMO: 2.79 vs 2.66

TXT: .74 vs .77

(reports after close, estimate provided):

AFL: 1.55

CDNS: .39

CTXS: 1.60

EBAY: .59

FB: 1.96

MDLZ: .56

MSFT: .86

PYPL: .52

QCOM: .90

SYMC: .44

T: .65

UNM: 1.08

VRTX: .58

Key Economic Reports

January ADP employment report released at 8:15am EST: 234,000 (actual) vs. 195,000 (estimate)

January Chicago PMI to be released at 9:45am EST: 64.0 (estimate)

December pending home sales to be released at 10:00am EST: +0.5% (estimate)

Happy trading!

Tom