Market Recap for Thursday, May 10, 2018

It was a very bullish day on Wall Street. I suppose you could nit pick and point to utilities (XLU, +1.41%) outperforming on an up day, but it's difficult to ignore the solid participation during yesterday's rise. All nine sectors were higher and the XLU simply saw a much-needed oversold bounce with the 10 year treasury yield ($TNX) and dollar (UUP) pausing for a change. Healthcare (XLV, +1.34%) and technology (XLK, +1.30%) also performed very well on the session. Within healthcare, medical supplies ($DJUSMS, +2.46%) was the leading industry group, but I have my eyes on health care providers ($DJUSHP, +1.67%), which also had a strong day. I see a very bullish inverse head & shoulders continuation pattern that, if executed (confirmed close above neckline resistance), would suggest a measurement to 2000, or approximately a 13% move higher from its current level. Here's the visual:

A continuation pattern requires a prior trend, which I believe is rather obvious above. While the consolidation that's taken place in the market since January is very frustrating, it requires patience to allow the market time to absorb additional supply as traders cash in their chips as volatility rises. I'm very much of the belief the consolidation period is winding down (or may have already wound down). Charts like the one of the DJUSHP above suggest plenty of upside potential in the coming weeks/months.

A continuation pattern requires a prior trend, which I believe is rather obvious above. While the consolidation that's taken place in the market since January is very frustrating, it requires patience to allow the market time to absorb additional supply as traders cash in their chips as volatility rises. I'm very much of the belief the consolidation period is winding down (or may have already wound down). Charts like the one of the DJUSHP above suggest plenty of upside potential in the coming weeks/months.

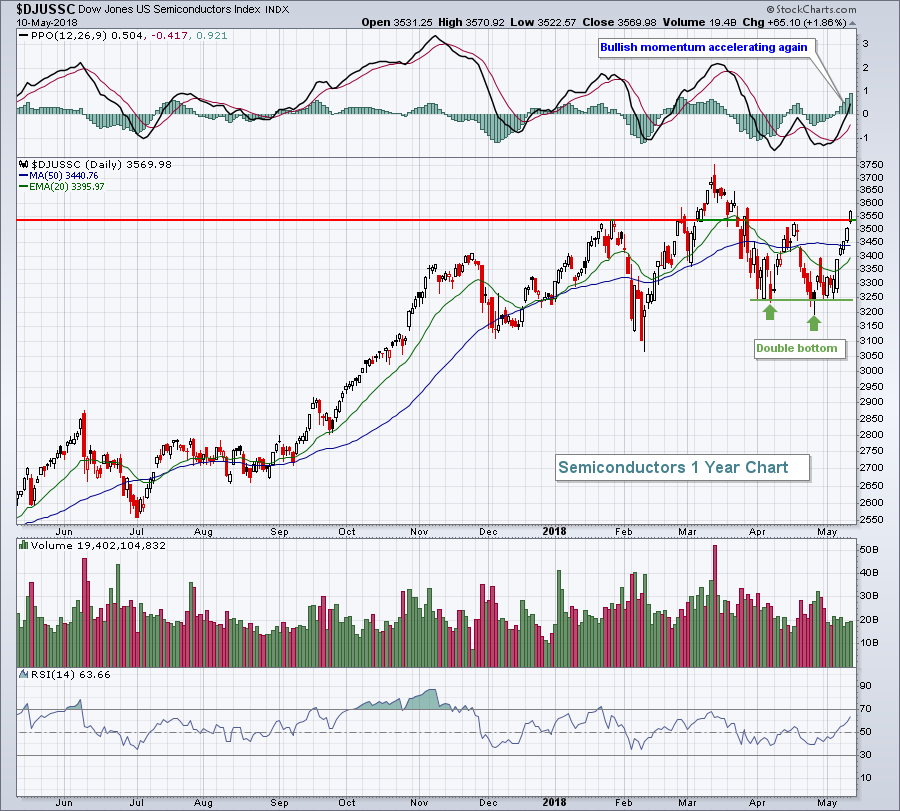

Technology got a lift from semiconductor shares ($DJUSSC). The DJUSSC closed at its highest level in nearly two months as NVIDIA Corp (NVDA) broke out to fresh all-time highs ahead of its quarterly earnings report, which was released after the closing bell on Thursday. Their results were exceptionally strong, but it does appear that some profit taking will kick in at the open. Check out the improved technical outlook for the DJUSSC, however:

Semiconductors were a big part of the bull market story in 2017 and it appears they're poised to resume their leadership role.

Semiconductors were a big part of the bull market story in 2017 and it appears they're poised to resume their leadership role.

Pre-Market Action

There's very little in the way of earnings or economic news today, so traders will be following the technical action closely. One index to watch closely will be the Russell 2000, where we've yet to see a close above 1611. Yesterday's intraday high reached 1609 so a break above 1611 today on the close should be respected.

The 10 year treasury yield ($TNX) and crude oil ($WTIC) are both near their respective flat lines this morning, with gold ($GOLD) rising moderately.

Asian markets were fairly strong overnight, but European markets have turned mixed this morning. Of note, the German DAX ($DAX) closed back above 13000 yesterday for the first time since the heavy selling began in late-January, and this index has been on a tear since bottoming roughly six weeks ago.

Here in the U.S., Dow Jones futures are up 24 points with 40 minutes left to the opening bell.

Current Outlook

The U.S. Dollar Index ($USD) paused on Thursday, but don't expect it to last long. U.S. treasury yields continue to climb at a much faster pace than Germany's and the USD has been playing catch up to the strengthening U.S. treasury yields since it bottomed in February:

Note that the U.S. 10 year treasury yield has broken out again vs. Germany's so the dollar's renewed strength is very likely to continue with more and more money rotating into small caps. That's a theme to consider for the balance of 2018, or at least for the foreseeable future.

Note that the U.S. 10 year treasury yield has broken out again vs. Germany's so the dollar's renewed strength is very likely to continue with more and more money rotating into small caps. That's a theme to consider for the balance of 2018, or at least for the foreseeable future.

Sector/Industry Watch

The Dow Jones U.S. Travel & Tourism Index ($DJUSTT) follows closely the price action of Booking Holdings (BKNG, formerly priceline.com). Unfortunately, BKNG did not get a great response from its quarterly earnings report as you can see below:

Price and gap support reside roughly in the 1975-2000 range so be careful if support there is lost - especially given BKNG's propensity to lose bullish momentum after April each year. For more on BKNG's historical tendencies, check out the next section below.

Price and gap support reside roughly in the 1975-2000 range so be careful if support there is lost - especially given BKNG's propensity to lose bullish momentum after April each year. For more on BKNG's historical tendencies, check out the next section below.

Historical Tendencies

Over the past 20 years, BKNG has risen during February, March and April 84%, 70% and 75%, respectively, of those years. Its average monthly gains for those three months have been 8.6%, 7.6% and 12.7%, respectively. But the buyers seem to dry up when May hits. From May through December, no month has risen more than 58% of the last 20 years and the average monthly gains for the last 8 months of the year are as follows:

May: +1.3%

June: +0.9%

July: -0.1%

August: +3.6%

September: -8.1%

October: +1.9%

November: +1.0%

December: -2.6%

If you add all of those months' gains together, you come up with -2.1%. It's as if the buying switch is turned off on BKNG as April comes to a close. I mention this because BKNG saw a less-than-stellar reaction to its earnings report yesterday and is approaching a key area of price support (see the chart above in Sector/Industry Watch section). It might be time to ring the register on this online giant and wait until later in 2018 to consider again.

Key Earnings Reports

(actual vs. estimate):

TRI: .28 vs .58

Key Economic Reports

May consumer sentiment to be released at 10:00am EST: 99.0 (estimate)

Happy trading!

Tom